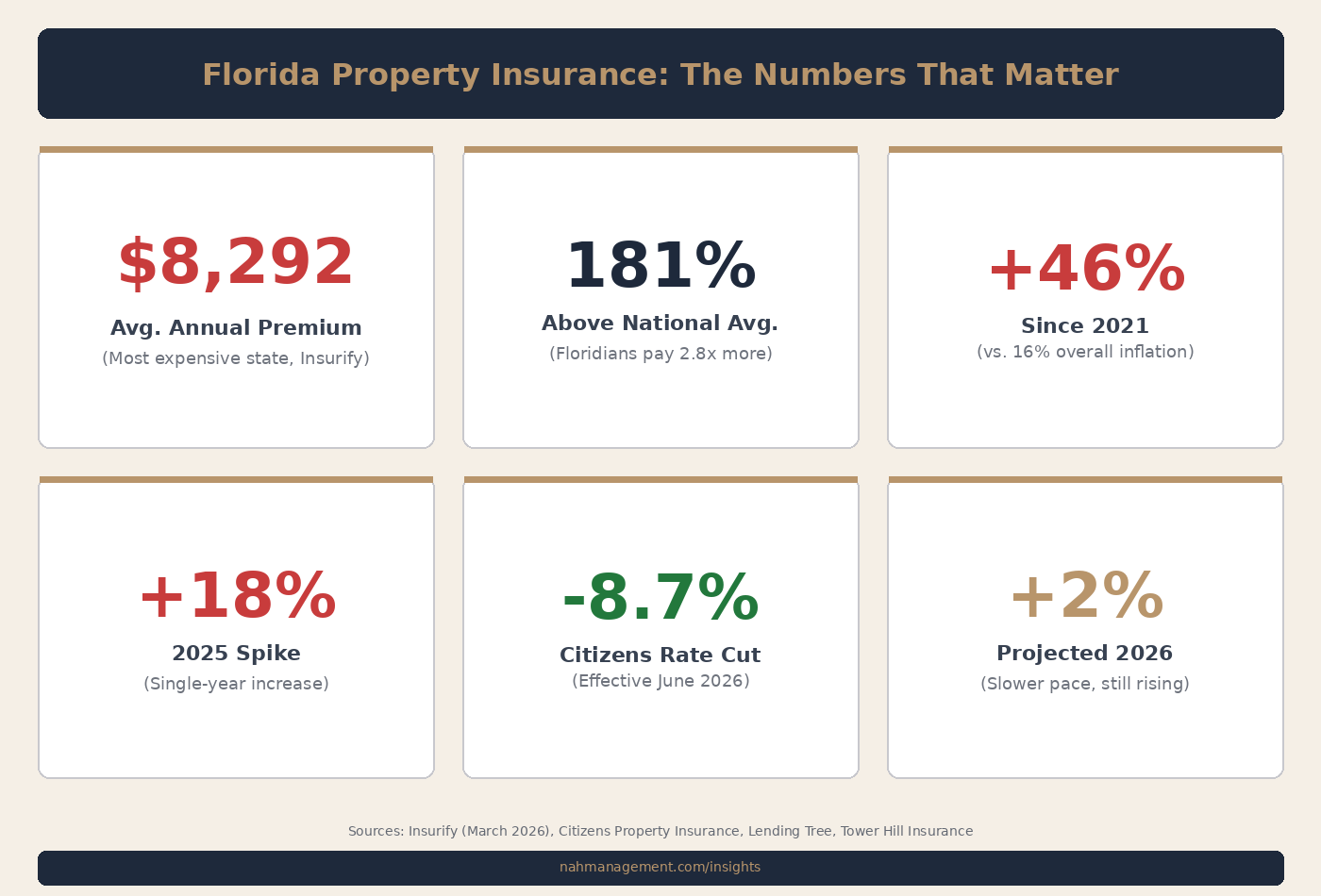

Florida homeowners now pay an average of $8,292 per year for property insurance, according to Insurify's March 2026 report. That makes Florida the most expensive state in the country for homeowners insurance, and it is not close: the second most expensive state, Oklahoma, costs approximately $3,000 less per year. For rental property owners in Central Florida, this is not an abstract number. It is a cost that has risen 46% since 2021, nearly three times faster than overall inflation, and it directly compresses the margin between gross rent and net operating income.

How Did We Get Here?

Florida's insurance crisis did not happen overnight. Premiums spiked 18% in 2025 alone, following years of compounding increases driven by a combination of factors that are unique to this state. Hurricane exposure is the most visible, but it is not the only driver. Rebuilding costs have surged alongside construction inflation: according to Tower Hill Insurance, what cost $400,000 to rebuild five years ago may now cost $600,000. Reinsurance, the insurance that insurance companies purchase to cover catastrophic losses, has also increased as global disaster events drive up costs worldwide. A wildfire in California or a typhoon in the Pacific can raise reinsurance premiums in Florida.

Florida also carried years of litigation-related losses that inflated claims costs far beyond the underlying damage. Legislative reforms passed in 2022 and 2023 addressed some of these issues, and the early results are measurable: Florida's domestic property insurers turned a profit in 2024 despite hurricane losses, and Citizens Property Insurance, the state's insurer of last resort, has reduced its policy count from a peak of 1.4 million in October 2023 to approximately 395,000 today. Citizens is also cutting rates 8.7% effective June 1, 2026.

Is the Market Stabilizing?

There are signs of improvement, but "stabilizing" does not mean "declining." Insurify projects premiums will rise another 2% by the end of 2026, bringing the average to approximately $8,458. That is a slower pace than the 18% increase in 2025, but it is still an increase on top of an already elevated base.

Florida Insurance Commissioner Mike Yaworsky has stated that the reforms have worked and that the state is creating a more stable marketplace. Matt Brannon, Insurify's Senior Economic Analyst, has noted that insurers may feel less urgency to raise rates in 2026 given the reforms and their improved financial footing. The trajectory is encouraging, but the absolute cost level remains the highest in the nation, and owners should plan accordingly.

Adding to the policy landscape, the Florida House unanimously approved HB 767 in February 2026, a transparency bill requiring insurers to explain premium increases in plain language, provide QR codes linking to a state consumer resource center, and disclose statewide average rate changes. The bill does not set or cap rates, but it does give property owners clearer visibility into why their premiums are moving.

"Insurance premiums in Florida have risen 46% since 2021, while overall inflation rose 16% over the same period. For rental property owners, this gap is not theoretical. It is the difference between a property that generates positive cash flow and one that does not."

Why This Matters More Than Most Owners Realize

Many generic investment calculators estimate annual insurance at $1,500 to $2,000 for a Florida property. The actual average is $8,292. That discrepancy alone can represent a $6,000 to $7,000 gap between projected and actual net operating income. For an owner evaluating whether to hold, sell, or invest in improvements, using the wrong insurance number leads to the wrong decision.

The math is straightforward. According to Lending Tree data, Florida insurance rates rose 49.5% from 2020 to 2025, while median household income climbed only 29.2% over the same period. Insurance costs are growing faster than the income base of the people paying them. For rental property owners, that means insurance is consuming a larger share of gross rent every year, and it requires active management, not passive acceptance.

What Owners Can Do About It

Insurance is not a fixed cost that owners have to absorb without recourse. There are specific actions that can reduce premiums, limit claim exposure, and protect net operating income.

Wind mitigation inspections. Florida law requires insurers to offer premium discounts for properties that meet specific wind mitigation standards. A certified inspection that documents roof-to-wall connections, roof covering type, secondary water barriers, and opening protection can produce meaningful savings. Many owners of older homes in Winter Park and surrounding neighborhoods have never had one done.

Roof condition and age. Roof age is one of the single largest variables in Florida property insurance pricing. A roof over 15 years old can trigger significantly higher premiums or even coverage exclusions. Owners who proactively replace or repair aging roofs are not just maintaining property value; they are directly managing their insurance cost.

Proactive maintenance that reduces claim risk. Water damage is among the most common and costly insurance claims in Florida. Properties with well-maintained plumbing, properly graded landscaping, sealed windows, and functioning drainage systems file fewer claims. Fewer claims mean lower premiums over time and fewer disruptions for tenants. This is one of the most direct ways that professional property management pays for itself.

Insurance claim coordination. When a claim does occur, how it is handled matters. Proper documentation, timely filing, coordinated contractor estimates, and clear communication with adjusters all affect the outcome. Mismanaged claims lead to underpayment, delays, and downstream premium increases that compound for years. At NAH Management, insurance claim coordination is one of our Concierge service categories specifically because we have seen how much value is left on the table when claims are handled reactively.

Florida insurance by the numbers. Sources: Insurify "Insuring the American Homeowner" Report (March 2026), Citizens Property Insurance, Lending Tree, Tower Hill Insurance.

The Connection to Rental Demand

Insurance costs do not exist in a vacuum. As we covered in our recent analysis of Orlando's population growth data, the region added 37,690 new residents in 2025, and 82% of that growth came from international migration. Many of these new residents will enter the rental market. That sustained demand supports occupancy and rent levels, but only for properties where the owner's cost structure is managed well enough to maintain positive cash flow after insurance, taxes, and maintenance.

A property generating strong gross rent can look very different after you subtract $8,300 in annual insurance, property taxes, maintenance, management, and vacancy. Owners who do not model these costs accurately, and update those models annually, are guessing. As we noted in our piece on what tenants actually pay for, the properties that perform best are the ones where the owner invests strategically, and insurance cost management is part of that investment.

What to Expect Going Forward

The trajectory is cautiously positive. Legislative reforms are producing results. Insurers are returning to profitability. Citizens is shrinking its book and cutting rates. The transparency requirements in HB 767 will give owners more visibility into how their premiums are calculated. But the absolute cost level, $8,300 per year and rising, is the baseline reality for the foreseeable future.

For rental property owners in Winter Park and across Central Florida, the practical response is not to wait for premiums to drop. It is to treat insurance as an actively managed operating cost: get wind mitigation inspections, maintain the property to reduce claim exposure, model the actual cost into financial projections, and work with a management team that understands how these costs flow through to net operating income.

Sources

Insurify, "Insuring the American Homeowner" Report, March 2026. WPTV News, April 13, 2026. Naples Daily News / Marco Island News, April 12, 2026. Bankrate State-by-State Insurance Rates, April 2026. Tower Hill Insurance, "Why Did My Home Insurance Go Up," February 2026. Florida HB 767, approved February 26, 2026. Lending Tree Florida Insurance Rate Analysis, 2020 to 2025. Citizens Property Insurance Corporation rate filings, 2026.