In my years working in institutional finance, one of the first things you learn is that no asset class operates in isolation. A disruption in energy markets moves bond yields. Bond yields move mortgage rates. Mortgage rates move housing affordability. And housing affordability moves every decision a property owner or tenant makes. The chain is always connected, even when the events at the start of it feel distant from the decision at the end.

That chain has been on full display over the past four weeks in the U.S. housing market, and its effects are reaching Central Florida in ways that matter for anyone who owns or rents residential property here.

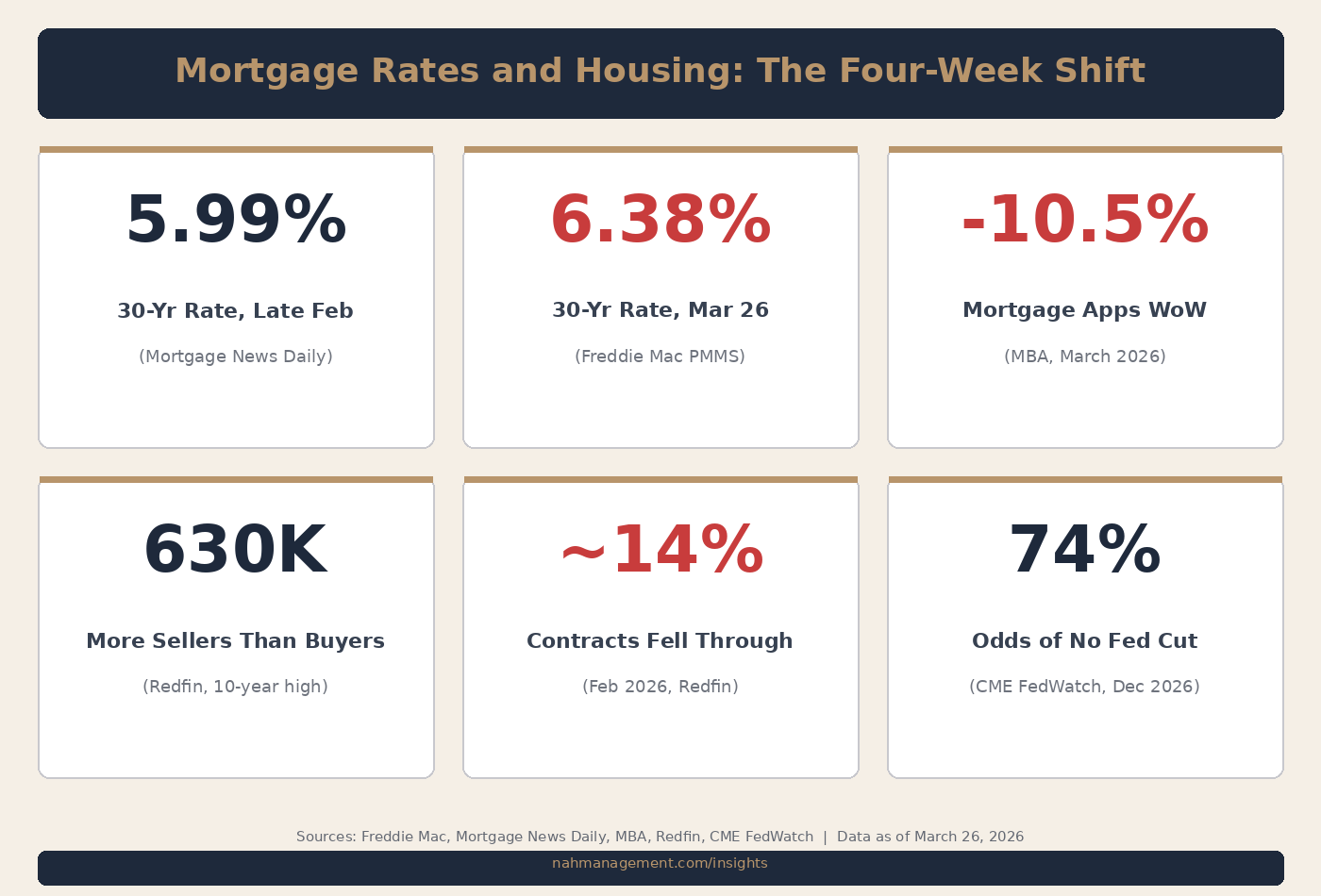

What Happened to Mortgage Rates

In late February, the average 30-year fixed mortgage rate fell below 6% for the first time since 2022, according to Mortgage News Daily. That threshold had long been viewed as a psychological turning point for both buyers and sellers. Economists widely expected it to bring renewed momentum to a housing market that had posted 30-year lows in transaction volume the prior year.

Source: Mortgage News Daily; CNN Business, February 26, 2026

The optimism was short-lived. By March 26, 2026, the Freddie Mac Primary Mortgage Market Survey reported the 30-year fixed rate had climbed to 6.38%, up from 6.22% the week prior. That represents four consecutive weeks of increases and the largest single-week jump since April 2025. Mortgage News Daily's daily index, which tends to track more current pricing, showed rates as high as 6.62% on the same day.

Source: Freddie Mac PMMS, March 26, 2026; Mortgage News Daily, March 26, 2026

The Chain Reaction

The mechanism behind this rate movement is straightforward, even if the events driving it are not. Mortgage rates are benchmarked to the yield on the 10-year U.S. Treasury note. When Treasury yields rise, mortgage rates follow. The 10-year Treasury yield climbed from approximately 3.96% before the current period of Middle East instability to 4.39% as of late March, according to Fortune, reflecting investor concerns about sustained inflation driven by elevated energy prices.

Source: Fortune, March 26, 2026; U.S. Treasury data

The connection to energy prices is direct. Disruptions to global oil supply routes have pushed crude prices sharply higher, which feeds into broader inflation expectations. When bond markets anticipate higher inflation, investors demand higher yields on Treasuries to compensate, which in turn pushes mortgage rates up. Susan Wachter, a professor of real estate at the University of Pennsylvania's Wharton School, explained the dynamic to Marketplace: "A key price for the inflation rate is oil. If oil markets are destabilized and oil prices continue to increase significantly, this is clearly going to raise the inflation rate."

Source: Marketplace, March 4, 2026 (Prof. Susan Wachter, Wharton School)

The Federal Reserve's posture adds another layer. At its March 2026 meeting, the Fed held its benchmark interest rate steady at 3.50% to 3.75% for the second consecutive meeting and signaled only one possible rate cut for the remainder of the year. Markets now place a 74% probability on rates remaining unchanged through December 2026, according to the CME FedWatch tool.

Source: Federal Reserve, March 2026 Meeting Statement; CME FedWatch Tool; IBTimes, March 26, 2026

The Immediate Housing Impact

The effects on buyer behavior have been swift. Mortgage applications fell 10.5% from the prior week, according to the Mortgage Bankers Association. Redfin reported that more than 42,000 homebuying contracts fell through in February, equal to nearly 14% of all homes that went under contract that month, the highest cancellation rate for any February since Redfin began tracking the data in 2017.

Source: Mortgage Bankers Association, March 2026; Redfin Contract Cancellations Report, February 2026

Redfin also reported that there are currently 630,000 more home sellers than buyers nationwide, the biggest gap in at least 10 years. Meanwhile, Freddie Mac's chief economist Sam Khater noted that despite the rate volatility, "the housing market continues to show gradual improvements compared to a year ago" and that both purchase and refinance applications remain up year-over-year.

Source: Redfin, March 2026; Freddie Mac PMMS Commentary, March 26, 2026

Key indicators as of March 26, 2026. Sources: Freddie Mac, Mortgage News Daily, MBA, Redfin, CME FedWatch.

The picture is nuanced. Rates are higher than they were a month ago, but still lower than this time last year, when the 30-year average was 6.65%. The market is under pressure, but it is not collapsing. It is adjusting.

What This Means for Central Florida Property Owners

For property owners in Central Florida, the rate reversal compounds trends we have been tracking closely. In our previous analysis, we documented a market that was already transitioning from transactions to operations: homes sitting on the market longer, prices softening, and owners increasingly choosing to hold and rent rather than sell.

Rising rates accelerate that transition in several ways.

The rate-lock effect intensifies. Owners who hold sub-4% mortgages from the pandemic era now face an even wider gap between their existing rate and current market rates. The financial incentive to hold rather than sell just increased. For many, converting to a rental continues to make more economic sense than selling into a buyer's market and refinancing at 6%+ on their next purchase.

Buyer demand weakens further. Higher rates reduce purchasing power. On a $450,000 home with 20% down, the difference between a 5.99% rate and a 6.38% rate amounts to approximately $1,120 per year in additional interest costs, or more than $33,000 over the life of a 30-year loan, according to CNN's calculation. That is enough to push marginal buyers back to the sidelines, which means more homes sit longer and more potential buyers remain renters.

Source: CNN Business, March 26, 2026

Rental demand holds steady or increases. Would-be buyers who cannot qualify or who choose to wait become renters. Even as rental supply has expanded in Central Florida (with Orlando rents down 4.3% year-over-year and statewide vacancy rising to 6.9%), the pool of renters is being replenished by buyers pushed out of the purchase market. This creates a more competitive tenant environment where the quality of the rental experience becomes a differentiator.

What This Means for Tenants

For tenants, the dynamics are mixed. More rental inventory is available, and rents have softened in many Central Florida submarkets. But the pipeline of new rental supply increasingly includes properties managed by owners who entered the rental market by circumstance rather than by strategy. As we noted in our previous article, not all new supply represents the same quality of living experience.

At the same time, tenants who were hoping to transition from renting to buying may find that timeline extended. Higher rates reduce what a buyer can afford at any given price point, which means some renters will stay in the rental market longer than they planned. For those tenants, the quality and stability of their current rental situation takes on greater importance.

What to Watch

The situation remains fluid. Several variables will shape how this plays out over the coming weeks and months.

Energy prices. The primary driver of the rate increase has been elevated oil prices flowing through to inflation expectations. If energy markets stabilize, the pressure on Treasury yields and mortgage rates could ease. If disruptions persist or deepen, rates could continue to climb.

Federal Reserve guidance. The Fed has signaled patience, but its stance will evolve with inflation data. Any shift toward rate cuts would provide relief to the housing market. The current market consensus, however, does not expect meaningful cuts in 2026.

Spring selling season. Historically, the housing market gains momentum in spring. Coldwell Banker CEO Kamini Lane told CNN there is "a lot of pent-up demand" and that stability in macroeconomic factors could still produce a healthy spring selling season. Whether that demand materializes will depend on how quickly rate volatility settles.

Source: CNN Business, March 26, 2026 (Kamini Lane, CEO, Coldwell Banker)

Local inventory and pricing. In the Orlando market specifically, the ORRA data through February 2026 showed inventory climbing and days on market extending. If rates remain elevated, sellers will face a choice between further price reductions and converting to rentals, both of which have implications for the local rental market's supply and quality mix.

The Operating Imperative

In a stable, appreciating market, property operations are a secondary concern. The asset does the work. In a volatile, transitional market like this one, operations become the primary lever. How quickly a vacancy is filled, how accurately a property is priced relative to the local market, how efficiently maintenance is managed, and how clearly performance is reported to the owner, these decisions compound over time and determine whether a property generates a meaningful return or simply breaks even.

For owners who are navigating this environment, the question is not just "what are rates doing?" It is "how well is my property being operated while rates do what they do?"

That is a question worth asking regardless of what happens next in global energy markets or at the Federal Reserve. It is also the question we built NAH Management to help answer.

If you own investment property in Central Florida, or work with clients who do, I welcome the conversation. Reach out through our website or connect with me on LinkedIn.