I understand the argument for a housing reset. Prices ran ahead of fundamentals, affordability is strained, and buyer demand has softened. But there is a key assumption embedded in the crash narrative: that sellers will accept large write-downs to clear the market. That is not what the data shows, and it is certainly not what we are seeing on the ground in Central Florida.

What is actually happening is more interesting, and more consequential for anyone who owns or operates rental property.

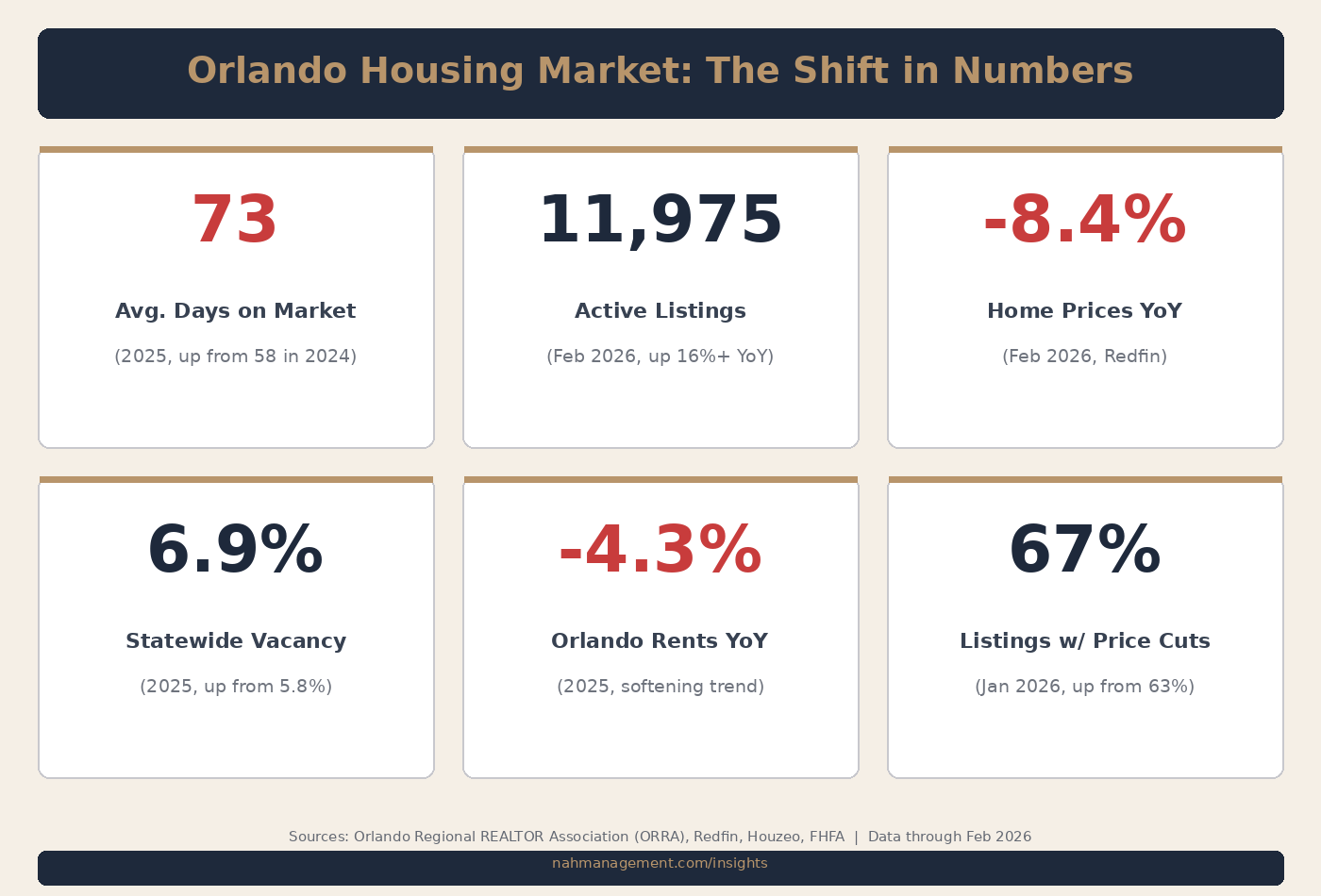

What the Numbers Tell Us

The Orlando Regional REALTOR Association reported that homes spent an average of 73 days on the market in 2025, up from 58 days in 2024. That is a 26% increase in time to sell, and the longest average since 2016. Inventory climbed to 11,975 active listings as of February 2026, up more than 16% year-over-year. The average monthly inventory in 2025 was 12,908, compared to 10,289 in 2024.

Source: Orlando Regional REALTOR Association (ORRA), 2025 Year-End Report and February 2026 Market Narrative

Redfin's February 2026 data for Orlando shows home prices down 8.4% year-over-year, with a median sale price of $376,000. Homes are selling after 71 days on average, up from 65 days last year. And according to Houzeo, 67% of Orlando listings had price reductions in January 2026, up from 63% the prior year.

Source: Redfin Orlando Market Data, February 2026; Houzeo Orlando Housing Market Report, January 2026

At the state level, the picture is equally telling. The FHFA House Price Index for Florida fell 2.3% year-over-year through Q3 2025, making it one of only a handful of states in negative territory while the national index rose 2.2%. January 2026 set a record for new listings in Florida, the most for any January going back to 2008.

Source: FHFA House Price Index, Q3 2025; Florida Realtors, January 2026 Market Data

These are not the indicators of a market about to snap back. They are the indicators of a market in transition.

The Behavioral Shift

If this were a typical correction, we would see distressed selling, foreclosure spikes, and rapid price capitulation. That is not the pattern. What we are seeing instead is a behavioral adjustment. Listings are sitting longer. Sellers are adjusting expectations more slowly. And many are choosing to convert to rentals instead of selling at a loss.

The rate-lock effect plays a role here. Many homeowners hold sub-4% mortgages from the pandemic era. Selling means surrendering that rate and entering a market where replacement financing costs significantly more. For these owners, holding and renting makes more economic sense than selling into a soft market.

"The question is no longer 'What can I sell this for?' It is becoming 'How does this asset perform if I hold it?'"

This shift is not hypothetical. Florida has added more than 50,000 new rental units over the past two years. Statewide vacancy rates rose to 6.9% in 2025 from 5.8% in 2024, driven by new multifamily delivery and owner conversions. Orlando rents fell 4.3% year-over-year as supply expanded.

Source: FHFA; Florida Rental Market Analysis; Orlando Regional REALTOR Association

Key market indicators through February 2026. Sources: ORRA, Redfin, Houzeo, FHFA.

From Transactions to Operations

The residential real estate market is quietly shifting from being transaction-driven to being operations-driven. For a generation, the dominant strategy was buy, hold for appreciation, and sell at a profit. The management of the asset during the hold period was secondary. Whoever collected the rent and coordinated repairs was good enough.

That model worked when appreciation alone could generate attractive returns. In a market where prices are flat to declining, vacancy is rising, and rents are softening, the quality of operations during the hold period becomes the primary driver of returns. The margin is no longer made on the buy or the sell. It is made on how the asset is operated while you own it.

The Gap That Creates

Most rental properties today are still not operated like assets. Pricing is inconsistent. Vacancy management is reactive. Maintenance decisions are often based on instinct rather than data. Financial reporting gives owners a disbursement amount but very little insight into how their property is actually performing against the market.

As more owners become reluctant landlords, entering the rental market without systems, without screening processes, and without operational infrastructure, that gap becomes more visible. A homeowner who never planned to be a landlord is now competing for tenants against professionally managed properties. The difference in experience for the tenant, and in financial performance for the owner, is significant.

| Metric | 2024 | 2025 / Early 2026 | Direction |

|---|---|---|---|

| Avg. days on market (Orlando) | 58 days | 73 days (2025 avg) | Homes sitting longer |

| Active inventory (Orlando) | ~10,289/mo avg | 11,975 (Feb 2026) | More options for buyers and tenants |

| Orlando rents | Flat to slightly up | Down 4.3% YoY | Softening as supply expands |

| Statewide vacancy | 5.8% | 6.9% | Rising with new supply |

| Listings with price cuts (Orlando) | 63% | 67% (Jan 2026) | Sellers adjusting downward |

| Home prices YoY (Orlando) | Flat to slightly positive | -8.4% (Feb 2026, Redfin) | Correction accelerating |

Sources: ORRA (2025 Year-End, Feb 2026 Narrative), Redfin (Feb 2026), Houzeo (Jan 2026), FHFA (Q3 2025)

What This Means for Owners

For owners who already hold rental property, the environment rewards operational discipline. In a market where rents are softening and vacancy is rising, the margin between a well-operated property and a poorly managed one widens. Pricing accuracy, tenant quality, maintenance efficiency, and cost containment all matter more when the market is not doing the heavy lifting for you.

For owners who are entering the rental market because selling no longer makes sense, the learning curve is steep. The difference between a property that generates a 6% net yield and one that generates 2% often comes down to operational decisions: how quickly a vacancy is filled, how tenants are screened, how maintenance is managed, and how the property is positioned relative to the local market.

What This Means for Tenants

More inventory entering the rental market sounds like unambiguously good news for tenants. In some ways it is: rents are softening, vacancy is up, and renters have more options than they have had in years. But more supply does not automatically mean better quality.

Many of the new rentals entering the market are managed by owners who never planned to be landlords. They lack screening processes, maintenance systems, and the operational infrastructure that makes a rental home function well for the person living in it. For tenants, the question is not just "can I afford this?" but "who is behind this property, and will they respond when something breaks?"

Looking Ahead

The ORRA president noted that interest rates dipped into the 5% range for the first time in February 2026, which may bring more buyers back into the market and ease some of the inventory buildup. Zillow projects a modest 1.2% price gain for the Orlando metro area over the next twelve months. The correction may be nearing its floor.

But even as the transaction market stabilizes, the structural shift toward rental operations is not going to reverse. The owners who converted to rentals during this period are not going to sell the moment prices tick up. They have become operators, whether they planned to or not. And the quality of those operations will determine who thrives in this market and who simply survives it.

If you own investment property in Central Florida, or work with clients who do, I am always interested in comparing notes on what this transition looks like in practice. The market is changing, and the owners who are paying attention to operations, not just valuations, will be the ones best positioned when it settles.

Reach out through our website or connect with me on LinkedIn.